Real Estate is one of the major sectors which has been deeply impacted by the COVID-19 pandemic and the consequent lockdown to contain it. The sector which was already seeing a lull period got hit by a ‘perfect storm’ of Coronavirus. If your company is seeing liquidity issues and cash flow mismatches and you are looking for an able advisor to help your company navigate through these stormy waters through a one-time restructuring, your search ends at InCorp.

Table Of Contents

Impact Of COVID-19 On Businesses

Need For A One-Time Restructuring Scheme

Who Is An Eligible Borrower For One-Time Restructuring Under This Framework?

Who Are Specifically Excluded (Not Eligible Borrowers) From This Framework?

What About Stressed MSME Accounts Having Borrowings Up To Rs. 25 Crore?

Are There Any Other Requirements / Compliances / Approvals Required For One-Time Loan Restructuring?

Will The Account Be Treated As NPA Due To The One-Time Restructuring?

How Does The One-Time Restructuring Impact The Financial Institutions?

When Can This Provision Be Reversed?

What Happens If The Borrower Defaults Even After One-Time Restructuring?

How Can InCorp Help You?

Impact of COVID-19 on Businesses

The economic impact of the COVID-19 pandemic has created significant stress on the liquidity and overall financial position of businesses, especially those which have a borrowing from banks, NBFCs and other financial institutions. The cashflow mismatches created to the subdued business activity over the last six months and the possibility of the same not recovering in the immediate future would lead to increasing rate of defaults by even otherwise viable and sustainable businesses.

The moratorium provided over the last six months, viz the period covering the lockdown phase in the country comes to an end in the current month and there was a need for addressing the issue of cashflow mismatch by a more sustainable and long term solution.

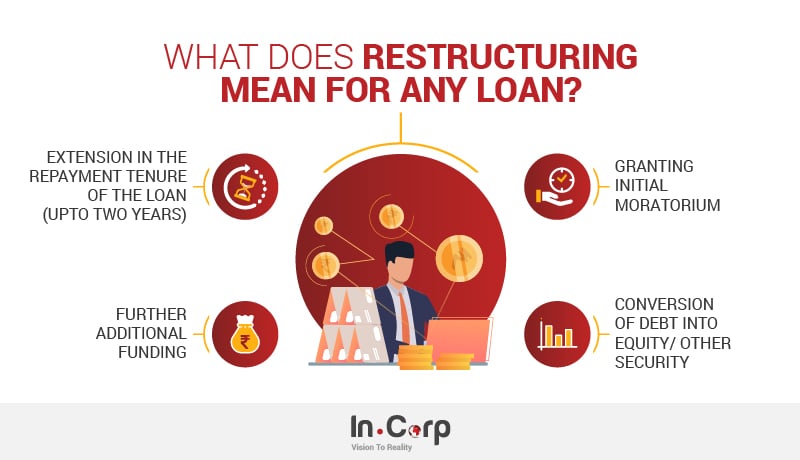

Need for a one-time restructuring scheme

There was a long-standing demand from the industry for RBI to announce a One-Time Restructuring of the loans to give much needed relief, clarity and long-term sustainable support to the businesses. The RBI announced a framework to permit restructuring of the stressed accounts of ‘eligible borrowers’ without the account being classified as a Non-Performing Asset (NPA)

This blog post highlights everything you need to know about a restructuring of loans; the eligibility criteria, the provisions involved and much more.

Who is an eligible borrower for one-time restructuring under this framework?

The following eligibility criteria must be satisfied to be an eligible borrower for loan restructuring under this framework:

- The borrower is under stress on account of COVID-19

- The borrower account is classified as ‘Standard’, but not in default for more than 30 days with any lending institution as on 1st March 2020. Further, the accounts should continue to remain standard till the date of invocation

- Further,

-

- In case of a single lender:

-

-

- The borrower and lending institution have agreed to proceed with a resolution plan under this framework not later than December 31, 2020

-

-

- In case of multiple lenders having exposure to the borrower:

-

-

- Lending institutions representing 75% by value of the total outstanding credit facilities (fund based as well non-fund based), and not less than 60% by number agree to invoke the resolution under this framework

- Resolution under this framework may be invoked on or before 31st December 2020 and must be implemented within 180 days from the date of invocation

- The resolution process is implemented when an ICA is signed by all lending institutions within 30 days from the date of invocation

- In case lending institutions representing not less than 75% by value of the total outstanding credit facilities (fund based as well non-fund based) and not less than 60% by number, do not sign the ICA within 30 days from the invocation, the invocation will be treated as lapsed. In respect of such borrowers, the resolution process cannot be invoked again under this framework

-

Who are specifically excluded (not eligible borrowers) from this framework?

The RBI Curricular states that the following borrowers / loans are specifically excluded from the one-time restructuring framework:

- MSME borrowers whose aggregate exposure to lending institutions cumulatively does not exceed Rs. 25 Crore as on 1st March 2020

- Farm Loans

- Loans to NBFCs, HFCs, Insurers and other financial service providers

- Loans to Primary Agricultural Credit Societies (PACS), Farmers’ Service Societies (FSS) and Large-sized Adivasi Multi-Purpose Societies (LAMPS) for on-lending to agriculture

- Loans to Central and State Governments; Local Government bodies

- Exposures of Housing Finance Companies

What about stressed MSME accounts having borrowings up to Rs. 25 Crore?

These MSMEs (whose cumulative exposure to banks & NBFCs including fund base and Non-Fund Based does not exceed Rs. 25 Crore as on 31st March 2020) were already covered under an earlier announced scheme under restructuring of loans vide circular dated 11th February 2020.

In view of the continued need to support the viable MSME entities on account of the fallout of Covid19, the RBI has decided to extend the scheme under the aforementioned circular whereby restructuring of the borrower account may now have to be implemented by 31st March 2021. However, the following conditions should be met:

- The MSME should have been classified as ‘standard asset’ as on 1st March 2020 and

- It should have obtained GST registration, unless it is exempt from obtaining the GST registration

- All other conditions under circular dated 11th February 2020 would be applicable

Are there any other requirements / compliances / approvals required for one-time loan restructuring?

In addition to the conditions set out to be an eligible borrower the following additional conditions are to be met in case of exposures above specific thresholds:

- In respect of accounts where the aggregate exposure at the time of invocation of the resolution process is Rs. 100 Crore and above, an independent credit evaluation (ICE) by any one credit rating agency (CRA) authorized by the Reserve Bank needs to be obtained

- In respect of loan accounts where the aggregate exposure of the lending institutions at the time of invocation of the resolution process is Rs. 1,500 Crore and above, an Expert Committee shall vet the resolution plans to be implemented under this window

- Further each lending institution shall frame its own Board approved policies pertaining to implementation of viable resolution plans for eligible borrowers under this framework

Will the account be treated as NPA due to the one-time restructuring?

The account will continue to be classified as standard and will not be downgraded to NPA so long as the conditions and repayments as outlined in the resolution plan approved under the framework are complied with. Hence there is no classification of NPA just because of the restructuring. This is a key relief provided under this framework.

How does the one-time restructuring impact the Financial Institutions?

The loan restructuring impacts the loans impacts the profitability, & thereby the capital adequacy ratios leading to reducing capacity to raise further funds, of the Financial Institutions since they are required to create a provision for the restructured loans. The provision required as follows:

- In case of personal loans – 10% of the residual loan or provisions held as per the extant IRAC norms immediately before implementation, whichever is higher

- For other loans where the lending institution has signed ICA within 30 days of invocation – 10% of the total debt or provisions held as per the extant IRAC norms immediately before implementation, whichever is higher

- For other loans where the lending institution has not signed ICA within 30 days of invocation – 20% of the debt on their books as on this date (carrying debt), or the provisions required as per extant IRAC norms, whichever is higher

When can this provision be reversed?

The financial institution may reverse the provisions as follows:

For the Institutions who have signed the ICA within 30 days of invocation:

-

- One half of the provision upon the borrower paying at least 20% of the residual debt without slipping into NPA post implementation of the plan

- Balance upon the borrower paying another 10% of the residual debt without slipping into NPA subsequently

For the Institutions who did not sign the ICA within 30 days of invocation:

-

- One half of the provision upon the borrower paying at least 20% of the carrying debt

- Balance upon the borrower paying another 10% of the carrying debt

What happens if the borrower defaults even after one-time restructuring?

All loans, other than the personal loans which are restructured under this framework, shall be subject to a monitoring period viz the period starting from the date of implementation of the resolution plan. This monitoring shall continue till the borrower pays 10% of the residual debt, subject to a minimum of one year from the commencement of the first payment of interest or principal (whichever is later) on the credit facility with the longest period of moratorium.

During the continuance of the monitoring period, if there is any default by the borrower with any of the signatories to the ICA, a review period of 30 days will be triggered. The borrower cannot default with any of the signatories to the ICA at the end of the Review Period.

If the borrower defaults, then the asset classification of the borrower with all lending institutions, including those who did not sign the ICA, shall be downgraded to NPA from the date of implementation of the resolution plan or the date from which the borrower had been classified as NPA before implementation of the plan, whichever is earlier.

How can InCorp help you?

Our team of experienced Investment Bankers & Resolution Professionals acting together as a single unit, provide a complete perspective to the lenders and stakeholders. We have raised over Rs. 2,200. Crs in the past 5 years and have also been involved in successful resolution of a real estate company having a loan of over Rs. 2,500 Crs. We are also currently assisting a few other real estate companies to resolve the liquidity issues faced by them.

We can help you in understanding the key nuances of debt restructuring and understanding of the one-time loan restructuring scheme. They can help you in exploring different options available to resolve the financial position of your business, evaluating the best course of action for your debt and also planning the execution of the entire restructuring process end-to-end.